We’ve all seen Chinese stocks explode in the last year; we’ve all seen margin lending soar to fund this exuberance; we’ve all read the dominant buyer in this trading frenzy is high-school-educated housewives; and we’ve all seen the analogs to the 2000 dotcom bubble. But, we guarentee you have never – ever – seen anything like this…

The number of new A-Share accounts opened just last week was a mind-boggling 3.25 million!!! That is double the number opened in the peak euphoria stage of the 2007 bubble…

This may not end well…

Charts: Bloomberg

We don’t mind being a little early rather than wrong when it comes to crashes. We’re not saying be out of stock markets as this Central Bank money printing madness may continue to be a winning hand for a while yet but it will pay to be diversified into quality assets.

Now back to the SDR story.

Last Monday there was a meeting in Washington hosted by the Official Monetary and Financial Institutions Forum (OMFIF) to discuss the future relationship, if any, of gold with the Special Drawing Rights (SDR).

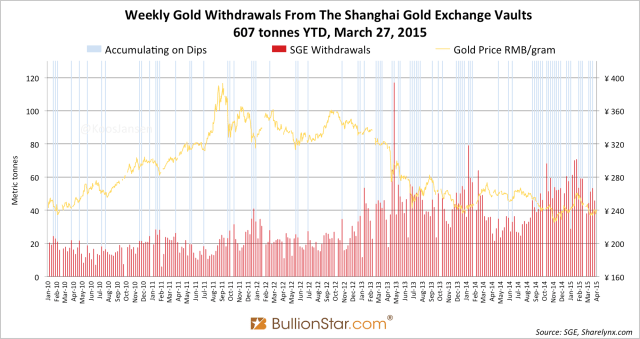

Also on the agenda was the inclusion of the Chinese renminbi, which seems certain to be included in the SDR basket in this year’s revision, assuming that the United States doesn’t try to block it.

This is not the first time the subject has come up. OMFIF’s chairman, Lord Desai wrote a paper about it after the last Washington meeting on gold and the SDR exactly four years ago. The inclusion of the renminbi in the SDR was rejected in 2010 because of inadequate liquidity and is due to be reconsidered this year.

Desai pointed out in his paper that there are difficulties when it comes to including gold, because (and I think this is what he was trying to say) none of the SDR’s paper constituents are convertible into gold, but gold’s inclusion in the SDR would make them convertible through the back door. However, Desai seemed keen to re-examine the case for gold.

It should be pointed out that if gold is included in SDRs the arrangement cannot be long-lasting so long as the major central banks insist on printing money as an economic cure-all. However, China’s position with respect to gold and her own currency could be a different matter.

The Chinese government has almost certainly accumulated large amounts of gold yet to be included in her reserves, and she has also encouraged her own citizens to own gold as well. We can therefore be certain that China sees a monetary role for gold while at the same time she is pushing for the renminbi to be included in the SDR basket. There is no doubt, if you read the IMF papers from the last SDR review in 2010 that the renminbi does now fulfil the criteria for inclusion today. So the question then is will the advanced nations, which dominate the IMF’s membership, permit the renminbi’s inclusion, and will the US, which has dragged its heels on giving China and the other BRICS nations a greater shareholding in the IMF, relent and permit these reforms, which were accepted by the other members back in 2010?

The Americans’ blocking of reform signals her desire to preserve the dollar’s hegemony; but given she lost out spectacularly over the creation of the Asian Infrastructure Investment Bank, IMF reform could become the next serious threat to the dollar’s dominance. And if America does not back down over the IMF and the SDR, she will have no fall-back position; China on the other hand still has some aces up her sleeve.

One of them is gold, and another is her role in a rival organisation established by the BRICS. The New Development Bank (NDB) is in the final stages of being set up, driven by frustration at America’s attempts to protect the dollar’s role and to keep the IMF as an exclusive club for advanced nations. Instead, the NDB could easily issue its own version of the SDR with the gold lining Desai referred to in his original paper.

The reason this would work is very simple. The BRICS members, unencumbered by the cost burden of modern welfare states could exercise the monetary restraint required to tie their currencies to gold, perhaps running a Bretton-Woods-style gold-exchange arrangement between member central banks to stabilise their currencies.

However, the NDB would almost certainly want to see the gold price considerably higher if it is to play any part in a new rival to the SDR. Other BRICS members would be encouraged to make sure they have sufficient gold on board by selling US dollar reserves to buy gold, ahead of any decision to go ahead with a new super-currency.

It would appear the era of the dollar’s global domination as a reserve currency is coming to an end, and the stage is now being set for gold to be officially accepted as the ultimate reserve money once again, this time by the next generation of advanced nations.

Recent Comments