Wolf Richter www.wolfstreet.com

Debt by Canadian households is a special phenomenon. Statistics Canada reported today that in the fourth quarter, household debt set another breath-taking record.

Earlier this month, even Equifax Canada, which is in the business of facilitating and increasing this indebtedness, had warned about it. The total indebtedness of Canadian households, according to its own measure, had jumped 7.7% from prior year, which had already been at record levels. The biggest culprits were installment and auto loans. Households are powering consumer spending, and thus the overall economy, with ever larger amounts of ultimately unsustainable debt.

A “a cautionary tale,” the report called it.

The rapid decline in oil prices caught many by surprise. And, that’s the point – consumers and business owners need to be more vigilant. When economic change happens, it can happen very quickly and can challenge previously observed stability of key economic and credit indicators.

In other words, as the price of oil collapsed, as housing stumbled, and as layoffs began – the “economic change” that “can happen very quickly” – the “stability” of different aspects of the economy, including household debt, is suddenly at risk. It’s a warning that consumers might buckle under that mountain of debt.

Now Statistics Canada weighed in. In Q4, household borrowing, on a seasonally adjusted basis, jumped by C$22.6 billion from the third quarter. Credit cards and auto loans accounted “for the majority of the overall increase.” Total household debt (consumer credit, mortgage, and non-mortgage loans) rose 1.1% from the prior quarter to C$1.825 trillion, with consumer credit hitting $519 billion and mortgage debt C$1.184 trillion.

And how did that impact households?

For the third consecutive quarter, disposable income increased at a slower rate than household credit market debt. As a result, leverage, as measured by household credit market debt to disposable income, reached a new high of 163.3% in the fourth quarter. In other words, households held roughly $1.63 of credit market debt for every dollar of disposable income in the fourth quarter.

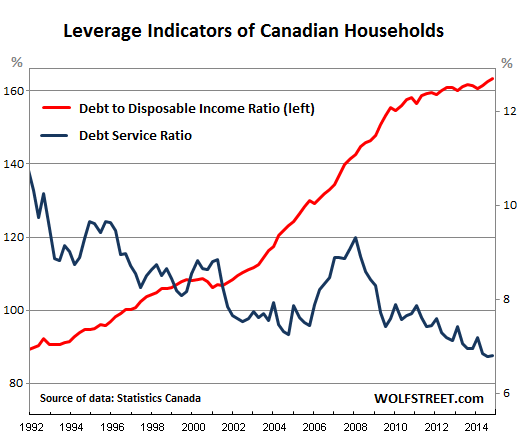

For the moment, there is still one saving grace to this rising mountain of debt: interest rates have been coming down for years. So the debt service ratio, which measures household interest expense as a proportion of disable income, has been declining as a function of interest rates, though it inched up in Q4 to 6.8%

The chart shows how the ratio of debt to disposable income (red line, left scale) has been rising with a few exceptions, while the debt service ratio (blue line, right scale) has followed interest rates up and down:

The ratio of debt to disposable income picked up speed from 2001 on. It blew through the financial crisis even as US households were whittling down their debt by deleveraging and defaulting. Canadian households didn’t even stop to breathe. They kept spending and piled on debt at an astounding rate. Their incomes rose also, but not nearly enough. It wasn’t until 2011 that the red-hot growth rate started to lose some of its fire, bumping into all sorts of resistance from reality.

With interest rates getting pushed lower year after year, interest expense as a percent of disposable income – the debt to service ratio – has been declining. For the moment, these low interest rates keep the whole thing glued together.

And if interest rates ever rise even by a smidgen? The blue line would do what it started doing in 2006. It would roar higher. With consumer indebtedness at these levels, even a small increase in interest rates will make a big difference in the interest expense consumers would have to fork over.

The Bank of Canada – kicked into panic mode by the collapse of oil prices, the faltering housing market, vulnerable banks, and other nagging issues, including the indebtedness of the consumer, which it pointed out as a risk factor last year – suddenly cut its benchmark interest rate in January. In the past, it communicated such moves in advance. In January, it was a surprise move that shocked the markets.

Today, Rhys Mendes, Deputy Chief of the Bank of Canada’s Economic Analysis Department, told the House of Commons finance committee that the central bank would “not necessarily” be pressured into following the Fed’s rate increases this year. “The bank targets inflation in Canada, and decisions regarding monetary policy in Canada would be based on the outlook for inflation,” he said, presenting the central-bank smokescreen for keeping rates at near zero for other reasons.

The Bank of Canada will have trouble ever raising rates, regardless of the distortion and mayhem near-zero rates are causing. Households can no longer afford higher rates. They have too much debt and not enough income. Higher interest payments would eat into spending on other things. Higher mortgage rates would crash the still magnificent home prices. Consumers would buckle under their burden and default. Not to speak of the already struggling oil companies. And then there are the banks that have lent with utter abandon to all of them.

Years of low interest rates encouraged this dreadful level of leverage. Now it’s an albatross around the neck of the Bank of Canada, and for decades to come. And for the economy, it’s a high-risk burden that could quickly, as Equifax suggested, blow up.

Gravity is already very inconveniently inserting itself into Canada’s incredible housing boom.

Recent Comments